)

Payroll and Super

Resources and information to help you to understand your obligations as an employer.

Hiring employees

- Checklist for small business owners to help you meet Australian laws when hiring an employee.

- All employees in Australia are entitled to a minimum wage and the 11 National Employment Standards (NES). Casual employees only get some of the NES entitlements.

- Awards, employment contracts, enterprise agreements and other registered agreements can't provide for conditions that are less than the National Employment Standards.

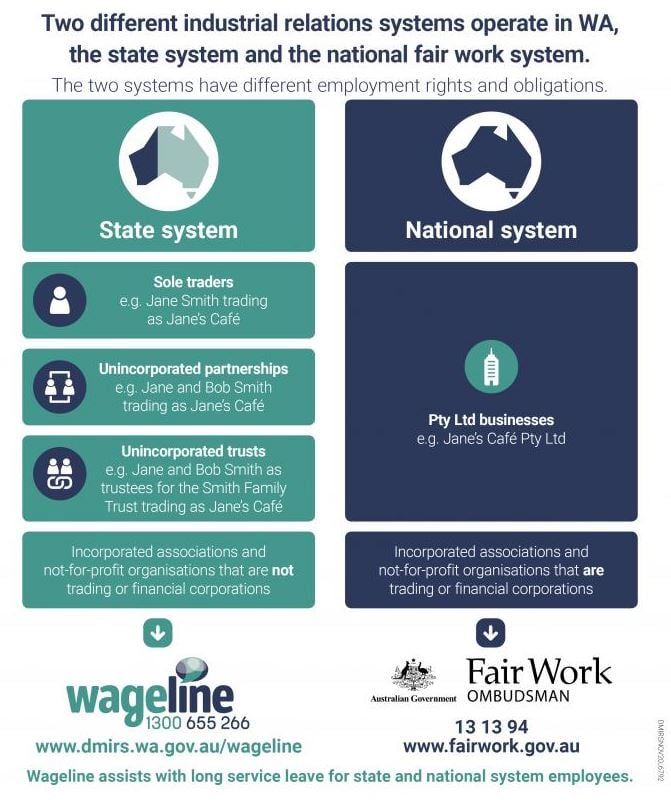

- For most employees, minimum pay rates and employment condtions are set out in the award which covers a particular industry or occupation. Employers in WA operating as sole traders, partnerships or unincorporated trusts are covered by the WA Industrial Relations system.

- Employers operating as a company structure (with Pty Ltd in their name) are covered by the national system. The relevant national award for your business and other valuable resources can be found on the Fair Work Ombudsman website.

- Awards set out minimum pay rates, hours of work, breaks, allowances, leave and super.

- An employer can draft their own enterprise agreement which sets out the conditions of employment for a group of employees. The pay rate cannot be less than the award.

- It’s a good idea to put your employee’s pay and conditions in writing in an employment contract.

- Employee or contractor? Generally, an employee works in your business and is part of your business. A contractor is running their own business. You are required to withhold tax from payments to contractors unless you have a valid ABN. If you do not comply with these withholding obligations you may be denied a tax deduction. Make sure you get a tax invoice and valid ABN.

Fair Work Ombudsman

- The Office of the Fair Work Ombudsman (FWO) is a statutory agency that assists employers and employees successfully navigate the Fair Work Act 2009 (The legislation that governs the employer/employee relationship).

- It is the role of the FWO to promote a well-balanced workplace and to ensure cooperative workplace relations.

- In addition, FWO also monitors, inquires into, investigates, and enforces compliance with Australia’s workplace laws.

- Fair Work Small Business Showcase includes a vast range of resources, tools and templates to assist small business owners.

- Latest news for small business.

Leave and entitlements

- You are required to give new employees a Fair Work Information Statement. Casual employees must also be give a Casual Employment Information Statement. Fixed term contract employees on a new contract must be given a Fixed Term Contract Information Statement.

- Your full-time and part-time employees are entitled to annual leave which begins to accumulate from the first date of their employment. The minimum entitlement for a full-time employee is 4 weeks for every 12 months worked.

- Your full-time and part-time employees are also entitled to personal leave (sick and carer’s leave). The minimum enttilement for a full-time employee is 10 days each year.

- Employees covered by the national (Fair Work) system are entitled to 10 days paid family and domestic violence leave in a 12 month period. (From 1/2/23 for employers with more than 15 employees. From 1/8/23 for employers with fewer than 15 employees).

- Eligible employees are entitled to 12 months of unpaid parental leave and can request an additional 12 months.

- Some awards require you to pay allowances to your employees, such as for uniform, work related items, travel expenses.

- Long service leave is a paid leave entitlement for employees who have long term continuous employment with the same employer. Many private sector employees in Western Australia are covered by the Long Service Leave Act 1958 (WA). Under the Long Service Leave Act, an employee may be eligible for long service leave when they leave a job after 7 years’ continuous employment, and may be entitled to take long service leave after 10 years’ continuous employment.

- Ending employment. Employment can end due to resignation, redundancy, end of contract or dismissal.

PAYG withholding

- You have to withhold tax from payments you make to your employees (PAYG withholding) in accordance with rates set by ATO and report the amounts in your activity statement (monthly or quarterly).

- This helps your employees to meet their tax liabilities at the end of the financial year.

- You must also withhold tax from other payments made to employees such as back payments, commissions and bonuses.

- There are special rules for some allowances and reimbursements.

Superannuation

- Employers are required to pay super (super guarantee) for their employees on top of their earnings to provide for their retirement. It applies to full-time, part-time and casual employees.

- The rate for pays paid after 1/7/23 is 11% of their ordinary time earnings ie your employee’s ordinary hours.

- Ordinary time earnings includes over award payments, commissions, shift loading, annual leave loading, allowances and bonuses.

- Overtime payments are not ordinary hours as long as they are distinctly identified as overtime.

- You are not required to pay super for employees under age 18 if they work less than 30 hours in a week.

- For pays paid prior to 1/7/22 you were not required to pay super for employees if they earned less than $450 before tax in a calendar month.

- You must offer your employees a choice of super fund by providing a super standard choice form. They can choose your default super fund.

- If your employee does not provide their choice of super fund you are required to request their stapled super fund details from ATO and pay into that fund (only for employees with start date after 1/11/21).

- If your employee does not have a stapled super fund you are required to pay into your nominated default super fund.

- Employers are required to report super to ATO for each pay event through Single Touch Payroll.

- You are required to pay the super each quarter in time for it to reach your employees’ super fund (or ATO clearing house) by the due dates: 28th Jan, 28th Apr, 28th Jul, 28th Oct. Allow at least 7 days for processing if using an alternative clearing house.

- You are required to pay super contributions electronically using a standard format known as the Superstream standard. This can be done either using an employer online account or a superstream clearing house eg ATO SBSCH, Beam, Xero.

- From 1/7/26 employers will be required to pay their employees' super at the same time as their wages. This measure, known as payday super, has been announced but is not yet law.

- If you do not meet your employer super obligations by the due date you are required to lodge an SG charge statement with ATO and pay the SG charge which includes severe penalties. For late payments, the super and the SG charge are not tax deductible.

Record keeping requirements

- You are required to provide payslips to your employees which include details for each pay period. These can be issued either electroncially or on paper.

- You must keep all records for your employees for at least 5 years, some records are required to be kept for 7 years after employment has terminated.

Payroll tax

Payroll tax is a self-assessed state tax, administered by RevenueWA, Department of Finance, paid by employers on taxable wages paid to employees.

- An employer is required to register for payroll tax as soon as taxable wages exceed the threshold amount of $1m in a financial year or $83,333 in a month.

- The amount of payroll tax payable is currently 5.5% of WA taxable wages in excess of a tax free threshold (deductable amount). The payment is generally tax deductible.

- The deductable amount is a diminishing threshold that gradually phases out between the annual threshold of $1m and $7.5m.

- Related businesses or businesses with common employees may be grouped for payroll tax purposes.

- Payroll tax returns are required to be lodged and paid monthly, due by 7th of the month.

- Payments can be made by direct debit, BPAY or EFT.

- An annual reconciliation return is due for lodgement by 21st July each year. (Includes June return).

- Exempt wages include apprentices registered under a training contract, workers compensation and reimbursement of business expenses.

- Employers are required to maintain proper books and records for a minimum of 5 years.

- Taxable wages include:

- Gross salaries and wages (includes leave)

- Commissions, bonuses and allowances

- Contractors/consultants (only for employer/employee relationships)

- Superannuation contributions (both salary sacrifice and super guarantee)

- Fringe benefits

- Directors’ remuneration

- Termination payments

- Specified taxable benefits (includes contributions to an industry redundancy fund or portable long service leave fund)

- Employee share acquisitions

Single touch payroll STP

- Single touch payroll ( STP) is the way employers report their employee’s payroll info (gross, tax and super) to the ATO.

- The required information is lodged with ATO each time your payroll is processed through your STP enabled software ie Xero, Quickbooks.

- STP started on 1 Jul 2019 for employers with 19 or fewer employees and is a mandatory obligation.

- Employees can access this information as year to date amounts via their myGov account.

- Employers are no longer required to provide payment summaries to their employees at year end

- Instead, you are required to lodge a finalisation declaration with ATO by 14th July.

- Employers can lodge an update event if they identify a need to amend details.

- The information will be displayed as a tax ready income statement for employees accessed through their myGov account.

- The information will also be pre-filled into their tax returns. paragraph.

STP phase 2

- STP phase 2 is the expansion of STP reporting for employers to report additional information to ATO.

- Information will be shared with various Government Departments including Services Australia (Centrelink, Child Support) and Fair Work.

- The start date was 1 January 2022. (Xero had a deferral in place until 31/3/23, MYOB until 31/12/22, Quickbooks commenced on 28/2/22).

- Additional information required to be reported includes:

- Disaggregation (breakdown) of gross amounts including separate reporting of bonuses, commissions, paid leave, allowances, overtime, salary sacrifice amounts, termination pay, directors fees, workers compensation and backpay for prior years.

- Separate reporting is only required if amounts are separately identified in an employment agreement.

- Separate reporting of paid leave is for time taken and paid. This can include annual leave, personal leave, long service leave, compassionate leave, cashed out leave, parental leave, community service, Jury duty and others.

- Separate reporting of allowances can include cents per km, award transport payments, laundry, overtime meals and travel in excess of ATO allowance, tools allowance, qualification, certification and task allowances if paid under an industrial instrument, and other allowances. (Excludes re-imbursements and fringe benefits).

- Employment basis and taxation conditions, including information from the TFN declaration and Medicare levy variations (Medicare surcharge variation, Medicare levy exemption or reduction).

- Income types eg working holiday maker (and home country) or closely held payee (directors, family members).

- Details of when and why employees leave your employment (eg voluntary, ill health, dismissal, contract cessation).

.JPG "ATO superstream")